Sep 17, 2010: market outlook

home faq articles premium contact

It has been very quiet on the finance.yendor.com front lately, but not for lack of engagement. I've been very busy improving PIE and making progress towards my end goal, namely: having a completely automated system that significantly outperforms the markets on a risk-adjusted basis.

Although it is a bit early to declare success, I think I've made a significant step forward. In the coming several months I will provide more details on the state of my current system, and my past 6 months "quiet period" journey.

Right now, I would like to share my outlook for the next few weeks.

The past 3 weeks: returns

We had a very impressive 3-week run-up in the markets. Just in case you're considering jumping in right now, I would like to advise caution. For full disclosure, I'm in 100% cash right now, and planning to get short, probably soon.

ETF 3-week %return OEF (iShares S&P 100) 7.20% SPY (SPDR S&P 500) 6.90% MDY (SPDR Midcap 400) 8.45% IWM (iShares Russell 2000) 8.54% QQQQ (Nasdaq 100 trust) 10.24% VWO (Vanguard emerging markets) 8.10% During the past 3 weeks rally, Thursday 2010-08-26, to Friday 2010-09-17, some key ETFs have had the following returns:

These are extreme moves for a 3-week period, by any measure.

The past 3 weeks: investor sentiment

Yesterday, the American Association of Individual Investors (AAII) bullish sentiment increased to 50.89% which is the second highest reading in two years. Contrast with merely three weeks ago, when bullish sentiment hit it second lowest reading in the last two years (source: Bespoke).Given these significant moves up, in both prices and sentiment, I believe we are now near, or already at, an intermediate term top with an expected correction that would bottom around the end of September or the beginning of October. The S&P500 could potentially fall by 6%-10%, with sectors like financials, and asset classes like small caps faring worse than the market due to their excess beta.

I'm still waiting for a final confirmation of this anticipated down-leg, as the major US indexes (DJI, S&P500 and the NASDAQ) are all still in up-trends.

The following charts should further explain my negative intermediate view:

A look into my market outlook model ensemble

First, is what my ensemble of multiple independent models, looking at over 200 ETFs (excluding short and leveraged ETFs) looks like at the end of trading on Friday, Sept 17, 2010.Think of it as a synoptic weather-map, with yellow being neutral (0% change), orange/red meaning "down" from here, and green/blue meaning "up" from here. The left edge of the chart represents a one day prediction from last Friday's close, and the right edge represents the 4-week (20 trading days) outlook with all the future 1-20 days in between.

As you can see, based on my system of models, there's a big "depression" moving towards us right now with the peak of the storm roughly 15 trading days (3-weeks) away:

Compare today's image to the same synoptic map, just 3-weeks ago, when markets were near a bottom, and most of what was seen 1-20 days ahead was optimistically green colored:What may be the most remarkable in the Aug 27 chart, is that it didn't just anticipate the upcoming big upside in the market in the first half of September, it also correctly predicted the roughly -1.5% drop in the market (orange area near the left edge) just before the run up started in earnest (Aug 30th).

Note that the recent rally (so far) has lasted a few days longer than the model originally anticipated. This is expected since no predictive market system is perfect. It is the nature of predictive models to have some inaccuracy.

The two heatmap charts were generated by my 'hm' heatmap tool using predictive data from multiple independent models I have developed over the past several months

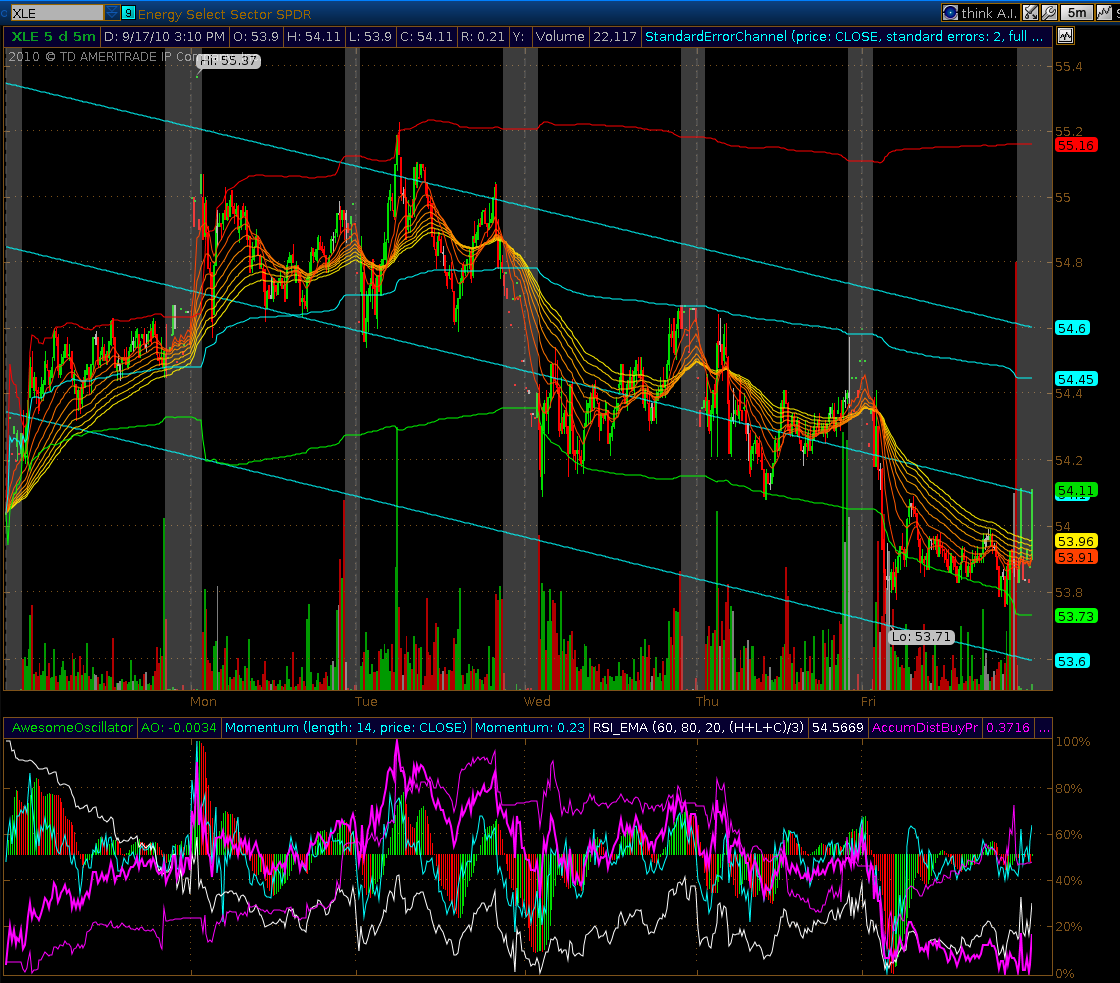

The 3 weakest S&P sectors

A reversal, should first be confirmed by the major indexes. Let's look at the weakest groups in the past week. These might be our down-leg leading indicators. As of Friday's close, 3 out of 9 S&P sectors: Energy (XLE), Materials (XLB), and Utilities (XLU) are already in 5-day down-trends after being nicely up in the past 3-weeks.

Are financials next?

A 4th sector: financials (XLF) has been making lower highs for 3 days, its 5-day VWAP has been declining for 3 days, and its 5-day average trend (straight blue regression lines) is now very close to a tipping point.

In summary

This is not a done deal. The markets could still end up next week. The final confirmation would come when the S&P500 as a whole turns negative on the 5-day chart, and 5 or more of its sectors are down-trending, with the VWAP and AccDist lines confirming the reversal from the extremely overbought run-up. Only at that point I would feel confident enough to short the market. Being ready is half the battle.For now anyway, caution is strongly advised. The downside risk far outweighs the upside.

The above merely reflects my own thinking and actions at the time of writing. Every investor should make up his own decisions based on his risk tolerance, time-frames, comfort-zones, convictions, and understanding. Never investment advice.

home faq articles premium contact

Any feedback is welcome.

-- ariel